30-Year Fixed at 6.49%: The Buy-Down Is the Real Lever for Denver

The 30-year fixed sits at 6.49% as of June 25, 2026. Here's the present-tense math on seller-paid buy-downs — and what Denver buyers and sellers should do about it.

As of June 27, 2026

I'm telling Denver buyers right now: stop negotiating the price and start negotiating the concession. The 30-year fixed is at 6.49% as of the week of June 25, 2026 — and at that rate, a seller-paid 2-1 buy-down delivers $790/month more payment relief in year one than the same dollars applied as a price cut. That's not a rounding difference. That's the whole negotiation.

The Rate This Week: 6.49% and What It Actually Means

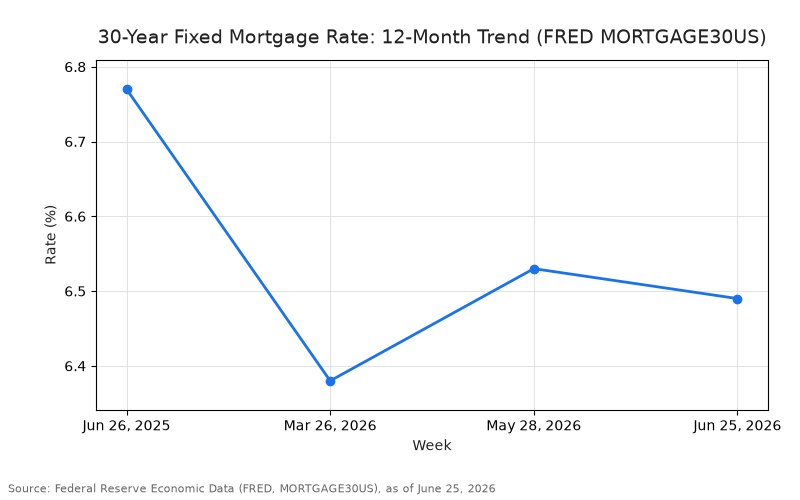

The 30-year fixed came in at 6.49% for the week of June 25, 2026, per FRED (MORTGAGE30US) [1]. That's down 28 basis points from 6.77% a year ago [2] — a meaningful improvement over the year-over-year window, though the near-term picture is choppier: rates are up 11 basis points from 6.38% in late March [1] and down just 4 basis points from 6.53% in late May [1].

Here's what that rate means in dollars: on a $750,000 Denver purchase with 5% down — a $712,500 mortgage — your monthly principal and interest payment at 6.49% is $4,499 [3]. That's $132/month less than you'd have paid at last June's 6.77% [4]. The year-over-year improvement is real. But the rate itself still creates a payment that stretches most buyers. That's exactly where the buy-down strategy earns its keep.

The Numbers: What 6.49% Costs — and What a Buy-Down Changes

Let's use the same scenario throughout: $750,000 purchase, 5% down, $712,500 mortgage, 30-year fixed at 6.49%.

At that rate, your payment is $4,499/month [3]. Now here's what a seller-paid 2-1 buy-down does to that number:

- Year one (rate: 4.49%): payment drops to $3,606/month — a $893/month reduction [6][8]

- Year two (rate: 5.49%): payment is $4,041/month — a $458/month reduction [6][8]

- Year three onward: payment steps back up to the full $4,499 at the 6.49% note rate [6][8]

The cost to the seller: approximately $16,212 — the total payment subsidy over those first two years [7].

Now compare that to the alternative. Take that same $16,212 and apply it as a straight price cut. The loan drops from $712,500 to $696,288, and the buyer's monthly payment falls by $103/month — permanently [9].

Same $16,212 from the seller. The buy-down delivers $893/month in year one. The price cut delivers $103/month. That's the math [10].

Why This Is the Negotiation Moment in Denver

Denver's detached single-family market in June 2026 is the setup this strategy was built for. The MSA-wide sale-to-list ratio sits at 0.999 [18] — buyers are negotiating fractionally below ask on average. Active inventory is down 7.2% year-over-year [14], so supply is tighter than it was, but the median days on market for detached homes is 37 days [13], and there's a meaningful stale-inventory tail: individual listings have sat for 201, 267, and 407 days [20][21][22], signaling that sellers on those properties have real motivation.

The median detached list price in the active Denver market is $800,000 [11], well above the MSA-wide all-property-type median of $589,000 [24]. At that price point, buyers are stretched — and sellers who want to move their listing have a tool that costs them roughly the same as a price cut but moves the buyer's payment far more.

This is a June 2026 Denver story, not a national one. The combination of moderate-but-not-distressed inventory, a 37-day median DOM, and a sub-1.0 sale-to-list ratio means sellers are competing for buyers — and the buy-down is the most efficient concession they can offer.

The Take: A Buy-Down Moves More Payment Per Dollar Than a Price Cut

Here's the reality: for the same $16,212 in seller help, a 2-1 buy-down delivers $790/month more payment relief in year one than an equivalent price reduction [10]. That's not a close call.

The temporary-vs-permanent trade-off is worth stating plainly, because it's actually a feature of the strategy, not a flaw. The buy-down front-loads the relief into years one and two — when a buyer is most stretched, carrying moving costs, furnishing a new home, and adjusting to a new payment [8]. By year three, the payment steps back to the fully-indexed 6.49% rate. The buyer knows this going in. That transparency is the whole point: you're not hiding anything, you're solving the right problem at the right time.

A price cut's $103/month relief is permanent — but it's also small enough that most buyers won't feel it. The buy-down's $893/month in year one is large enough to change the decision. That's why it closes deals.

No forward market call needed here. This strategy works at today's rate regardless of where rates go. If rates fall and the buyer refinances in year two, they've captured the buy-down benefit for the period they needed it most. If rates stay flat, they've had two years of materially lower payments. Either way, the math at closing favors the buy-down over the price cut.

What It Means for Denver Buyers and Sellers

If you're buying at today's 6.49% rate, a seller-paid 2-1 buy-down is a legitimate, present-tense negotiating ask — not an exotic request. On a $750,000 purchase, you're asking the seller to fund approximately $16,212 in concessions structured as a buy-down rather than a price reduction. In exchange, your year-one payment drops from $4,499 to $3,606 — $893/month back in your pocket when you need it most [6][8]. In a market where the sale-to-list ratio is 0.999 [18] and stale listings are sitting for months [20][21][22], this is a reasonable ask on the right property.

If you're selling, a buy-down concession is worth understanding before you default to a price cut. The Denver detached median is $800,000 [11] and buyers at that price point are payment-sensitive. Offering $16,212 as a buy-down instead of a price reduction costs you roughly the same net — but it moves the buyer's payment by nearly nine times as much in year one [10]. On a listing that's been sitting, that's the difference between a deal and another week on market.

Run the Real Numbers on Your Denver Purchase or Sale

We run this math for our clients every week — the buy-down cost, the year-one savings, the break-even against a price cut, all of it specific to your purchase price and down payment. If you're buying or selling in Denver and want to see how this works on your actual numbers, reach out directly. No rate speculation, just the math that applies to your situation today.

---

Paul McCoy, Realtor | Fathom Realty | License #: FA.100105533 | (319) 325-0668 | pmccoy626@gmail.com

Paul McCoy is a licensed real estate professional in Colorado. Equal Housing Opportunity.