Cost of Living in Denver: What Relocating Buyers Actually Need to

Planning a move to Denver? Here's what housing, taxes, insurance, and daily expenses actually cost — with real numbers for buyers, not generic index tables.

Most cost-of-living guides for Denver will hand you an index number and call it a day. That's not useful if you're actually buying a home here. What you need is a line-by-line breakdown of what ownership costs — mortgage, taxes, insurance, maintenance, and the Denver-specific surprises that don't show up until after closing.

Here's the reality: Denver is not cheap, but it's also not the coastal-metro price level that many relocating buyers fear. The gap between what you're imagining and what you'll actually pay depends almost entirely on where you're coming from — and which line items you're accounting for.

The five largest inbound relocation states to Denver are California, Texas, Florida, Arizona, and Illinois, in that order. Each of those markets has a different cost structure, and Denver compares differently against each one. This guide walks through every major budget line so you can build a real number before you start touring homes.

Why Denver's Cost of Living Surprises Most Relocating Buyers

The surprise usually cuts both ways. Buyers arriving from California or the New York metro often expect Denver to feel like a bargain — and on housing, it can be. Buyers arriving from Texas, Arizona, or the Midwest sometimes expect Denver to be comparable to what they're leaving, and find the housing costs higher than anticipated.

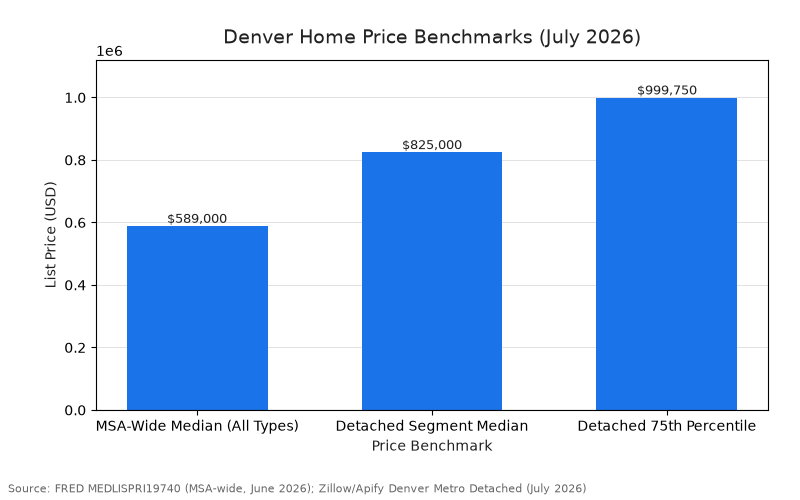

The Denver Metro detached home market is currently sitting at a median active list price of $825,000, with the 75th percentile at $999,750 — meaning upper-tier buyers are shopping right at the edge of seven figures.[1] The MSA-wide median across all property types (condos and townhomes included) is $589,000.[2] Median days on market for detached homes is 43 days, and the MSA-wide sale-to-list ratio is 0.999 — buyers are negotiating modest discounts below asking, not bidding above list.[3]

That's the housing headline. But housing is only part of the picture. Colorado's tax structure, insurance costs driven by hail and altitude, and a handful of Denver-specific environmental factors all shape what you'll actually spend each month. The buyers who get surprised are the ones who modeled housing and stopped there.

Housing: The Biggest Line Item in Any Denver Budget

Housing is where your budget either works or doesn't. At the detached median of $825,000, you're looking at a meaningful mortgage regardless of your down payment. At the MSA-wide median of $589,000 — which includes condos and townhomes — the math is more accessible, but still requires careful planning.

Here's what the current rate environment looks like in concrete terms. The 30-year fixed mortgage rate is 6.43% as of early July 2026, down 24 basis points from a year ago.[4] On the $589,000 MSA-wide median with 5% down, that's a $559,550 mortgage and a monthly principal-and-interest payment of $3,511.[5] Bring 20% down ($117,800) and the mortgage drops to $471,200 with a monthly P&I of $2,957 — a $554/month difference that makes a real case for saving toward the larger down payment if you can.[6]

For buyers targeting detached homes at the $825,000 median, the mortgage scales accordingly. A 5% down payment leaves a mortgage well above the MSA-wide reference loan — budget your P&I from the $825,000 starting point, not the all-property-types median.

Property taxes are one of Denver's genuine advantages. Colorado's effective property tax rate is approximately 0.50% of market value statewide — among the lowest in the nation.[7] Colorado reassesses to current market value (unlike California's Prop 13 freeze, which caps assessed value on long-held properties), so your tax basis will reflect what you paid. But at 0.50%, the annual tax burden on a $589,000 home is meaningfully lower than what buyers from high-tax states are used to carrying.

Homeowners insurance in Colorado runs higher than the national average, driven primarily by hail exposure. Colorado is one of the most hail-active states in the country, and insurers price that risk into premiums. Budget for insurance costs above what you'd pay in a lower-risk state — the exact premium depends on your specific property, roof age, and coverage level, but don't use a national average as your benchmark here.

HOA fees are common in Denver, particularly in newer developments, townhome communities, and condo buildings. If you're buying in a community with an HOA, add that monthly figure to your housing cost calculation before you compare neighborhoods. HOA fees in Colorado communities can range from modest to substantial depending on the amenities and the age of the community's infrastructure.

Taxes: What Colorado's Structure Means for Your Take-Home Pay

Colorado's tax structure is one of the cleaner stories in this budget guide — it's straightforward and, for most relocating buyers, favorable.

State income tax: Colorado levies a flat 4.40% on all taxable income (tax year 2025).[8] There are no brackets, no phase-outs, no surprises. If you're coming from California, where the top marginal rate reaches 13.3% and the 9.3% bracket applies to a broad range of incomes, the difference is substantial. If you're coming from Texas or Florida — which have no state income tax — Colorado's 4.40% is a new line item, but it's a predictable one.

Property taxes: As noted above, Colorado's approximately 0.50% effective rate is among the lowest nationally.[7] Colorado reassesses to current market value, so your assessed value will track your purchase price — but the rate itself is low enough that the annual bill stays manageable relative to what buyers from California, Illinois, or the Northeast are accustomed to paying.

No estate tax, no inheritance tax: Colorado has neither a state estate tax nor an inheritance tax.[9] For buyers relocating from states with separate estate-tax layers, this is a meaningful long-term benefit.

Sales tax: The combined sales tax in the City and County of Denver is 9.15% — Colorado state at 2.90%, RTD at 1.00%, Cultural Facilities District at 0.10%, and Denver city at 5.15%.[10] That's higher than California's statewide 7.25% base rate, so buyers arriving from California will notice the difference at the register.

The net picture: Colorado's income and property tax structure is favorable for most relocating buyers. The sales tax in Denver proper is on the higher end. Run your own numbers against your current state's structure — the comparison almost always favors Colorado on income and property taxes.

Everyday Expenses: Groceries, Transportation, and Utilities

Denver's everyday costs — groceries, gas, utilities, dining — run modestly above the national average. It's not a coastal-metro price level, but it's not a low-cost-of-living market either. Buyers arriving from California or the New York area will find everyday expenses noticeably lower. Buyers arriving from Texas, Arizona, or the Midwest may find them comparable or slightly higher.

A few line items that catch relocating buyers off guard:

- Utilities: Denver's altitude and climate mean heating costs in winter and, increasingly, cooling costs in summer. Air conditioning is standard in newer construction but less universal in older Denver homes — verify before you buy. Utility costs vary significantly by home size, age, and insulation quality.

- Transportation: Denver is a car-dependent metro outside of a handful of walkable urban neighborhoods. Budget for a car (or two) unless you're specifically targeting LoHi, RiNo, or Cherry Creek, where walkability and transit scores are meaningfully higher. Gas prices in Colorado track national averages closely.

- Dining and entertainment: Denver's restaurant scene has grown substantially over the past decade. Prices at mid-range and upscale restaurants are in line with other major metros — not the bargain some buyers expect relative to coastal cities, but also not the premium of a coastal metro.

- Altitude adjustment: Denver sits at 5,280 feet above sea level.[11] For buyers arriving from sea level, physiological acclimation — mild dehydration, sleep changes, exercise tolerance — typically takes two to four weeks. It's not a budget line item, but it's worth knowing before you arrive.

How Denver Compares to Where You're Coming From

The five largest inbound relocation pipelines to Denver's eight-county metro, per IRS migration data for the 2022–2023 tax year, are California (approximately 11,776 people), Texas (approximately 10,486 people), Florida (approximately 5,605 people), Arizona (approximately 4,264 people), and Illinois (approximately 3,381 people).[12]

Each of those origin markets compares to Denver differently:

California: The housing cost arbitrage is the primary driver. California's coastal metro prices run well above Denver's — high-equity California sellers often arrive in Denver with substantial down payments and find their purchasing power stretches further here. Colorado's 4.40% flat income tax rate sits well below California's top marginal rate of 13.3%, and Colorado's 0.50% effective property tax rate compares favorably to California's effective rate of around 0.71% (and California's Prop 13 caps prevent reassessment on long-held properties, while Colorado reassesses to current market value).[13] The tax arbitrage is real and durable for high earners.

Texas and Florida: Both states have no state income tax, so Colorado's 4.40% flat rate is a new cost. On housing, Denver's detached median of $825,000 is above many Texas and Florida markets, though the comparison varies significantly by submarket. The property tax picture is more nuanced — Texas property taxes are notably high, so Colorado's 0.50% effective rate is a meaningful improvement for Texas buyers.

Arizona: Phoenix and Tucson buyers will find Denver's housing costs higher, particularly in the detached segment. Arizona's income tax structure has been moving toward a flat rate in recent years; the comparison to Colorado's 4.40% depends on current Arizona rates at the time of your move.

Illinois: Chicago-area buyers often find Denver's housing costs comparable in the mid-range and higher in the upper tier. Illinois has a flat state income tax rate, and Cook County property taxes are among the highest in the nation — Colorado's 0.50% effective rate is a substantial improvement for Illinois buyers carrying high property tax bills.

One closing note on insurance: Colorado's hail exposure means homeowners insurance premiums run higher than in most of the origin states above. Factor that into your comparison — it partially offsets the property tax advantage.

Ownership Costs That Don't Show Up in the Listing Price

This is the section most buyers skip, and it's where the real surprises live. Denver has several ownership cost factors that are either unique to this market or more pronounced here than in most origin states.

Radon: Colorado has one of the highest radon concentrations in the country. The Colorado Department of Public Health and Environment reports that about 44% of results from more than 168,000 Colorado tests measure at or above the EPA's 4 pCi/L action level — and the EPA places Denver-metro counties (Denver, Adams, Arapahoe, Boulder, Broomfield, Douglas, Jefferson) in Zone 1, its highest radon-potential category.[14] Budget for a radon test as part of your inspection, and budget for mitigation if the test comes back elevated. Mitigation systems are a known, manageable cost — but you need to test first.

Expansive soils: The Denver metro sits on widespread expansive (swelling) clay soils. The Colorado Geological Survey identifies these formations as one of Colorado's most significant and costly geologic hazards: the soil swells when wet and shrinks when dry, stressing foundations over time.[15] Foundation movement is a common finding in Denver-area home inspections. If you're buying a home built before the mid-1990s, pay close attention to the foundation section of your inspection report and the seller's disclosure.

Hail: Colorado is one of the most hail-active states in the country, and the Denver metro sits in a high-frequency corridor. Hail damage to roofs is the single largest driver of homeowners insurance claims in Colorado — and insurers price that risk accordingly. When you're evaluating a home, ask about the roof age and material. A newer impact-resistant roof can meaningfully reduce your insurance premium; an aging roof is a near-term replacement cost to budget for.

Home inspection and due diligence: Colorado real estate transactions close through title companies, not attorneys — a workflow difference for buyers arriving from attorney-closing states like New York, New Jersey, or Massachusetts.[16] The inspection objection deadline in Denver-area contracts is a negotiated date, commonly set around 7 to 10 calendar days from acceptance — more compressed than California's 17-day default contingency period.[17] Budget time and attention for due diligence; the timeline moves faster here.

Ongoing maintenance: A standard rule of thumb for annual home maintenance is roughly 1% of the home's value per year. At Denver's detached median of $825,000, that's a meaningful annual reserve. Budget for it from day one — Denver's climate (freeze-thaw cycles, hail, UV exposure at altitude) is harder on exterior surfaces than many buyers expect.

What This Means for Your Buying Budget

Here's how to build a realistic Denver ownership budget from the numbers in this guide:

Start with the mortgage. At the MSA-wide median of $589,000 with 5% down, your monthly P&I at today's 6.43% rate is $3,511. With 20% down, it drops to $2,957.[5][6] For detached homes at the $825,000 median, scale from there. The 30-year fixed is 24 basis points lower than a year ago — buyers who lock now carry a lower payment for the life of the loan than buyers who locked a year ago.[4]

Add property taxes. Colorado's approximately 0.50% effective rate is one of the lowest in the nation. On a $589,000 home, that's a manageable annual figure — well below what buyers from Illinois, New Jersey, or Texas are used to paying.

Add insurance. Budget above the national average for homeowners insurance given Colorado's hail exposure. Get a quote specific to the property before you close — roof age and material matter significantly.

Add HOA if applicable. Many Denver communities carry HOA fees. Verify before you make an offer; the monthly HOA cost is a real line item in your housing budget.

Reserve for maintenance. The 1%-of-value annual maintenance rule is a reasonable starting point. Denver's climate and the expansive-soil foundation risk mean this reserve is not optional — it's a real cost of ownership here.

Account for the tax shift. If you're coming from a no-income-tax state, Colorado's 4.40% flat rate is a new line item. If you're coming from California or Illinois, it's a meaningful reduction. Run your own scenario.

The buyers who navigate Denver's cost of living well are the ones who model all of these line items before they start shopping — not after they're under contract. Explore your Denver neighborhood options and review what buyers need to know before making an offer to get oriented before you run the numbers.

Ready to Run the Real Numbers for Your Move to Denver?

If you're relocating to Denver and want a budget built around your specific price point, down payment, and origin market — not a generic index table — I'll do a quick, no-commitment budget review with you. We'll work through the mortgage math, the tax comparison to where you're coming from, and the Denver-specific ownership costs that most buyers don't find until after closing.

Check current Denver market conditions to see where the market stands right now, then reach out directly: pmccoy626@gmail.com or (319) 325-0668.

---

Paul McCoy, Realtor | Fathom Realty | License #: FA.100105533 | (319) 325-0668 | pmccoy626@gmail.com

Paul McCoy is a licensed real estate professional in Colorado. Equal Housing Opportunity.